Kevin Tynan, Director of Research

ktynan@thepresidiogroup.com

Without one-time catalysts pushing new-vehicle sales, dealers will rely on other business lines to drive revenue growth in 2026

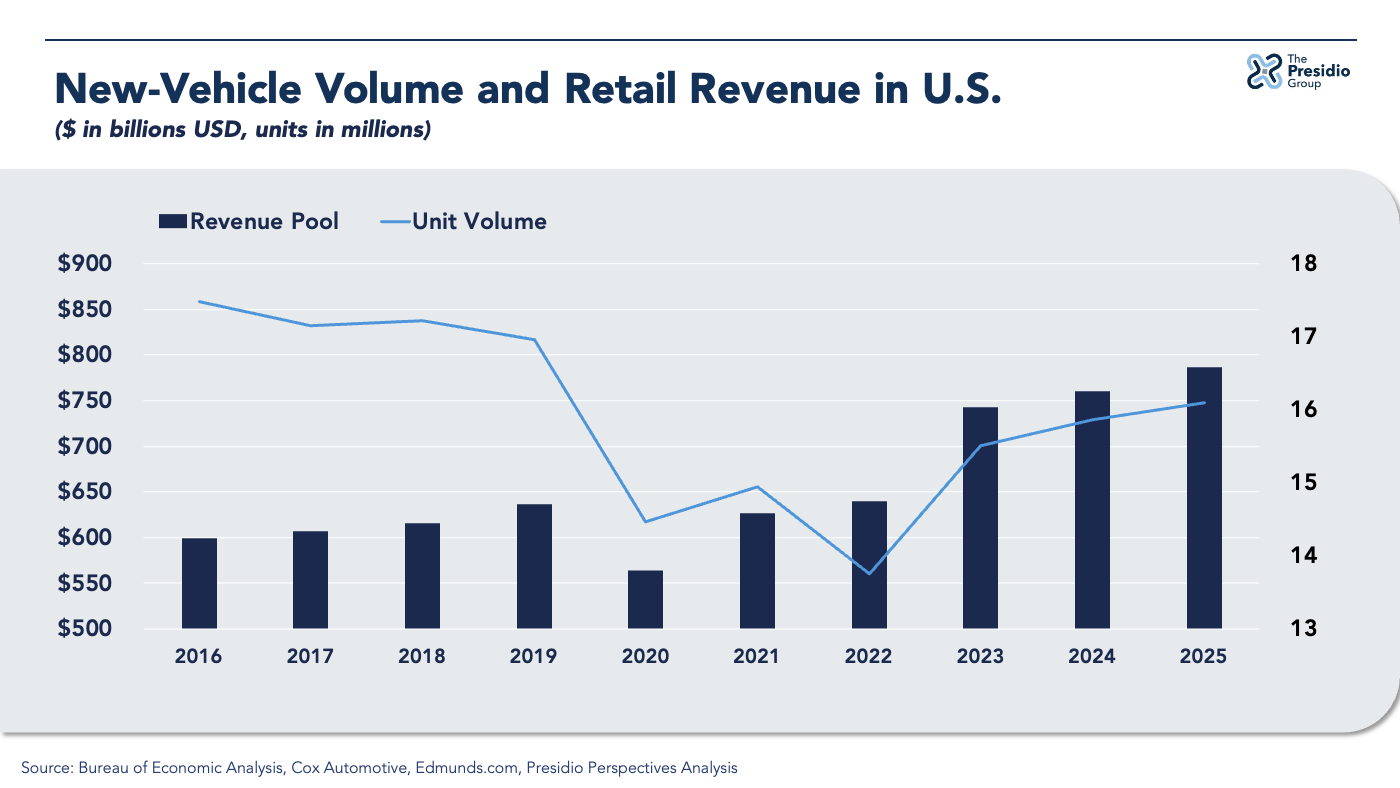

Franchised auto dealers may need to lean more heavily on their revenue diversity in 2026 as the factors that drove U.S. new-vehicle sales to an estimated 16.3 million units in 2025 — namely the specter of higher tariffs and expiring electric vehicle tax credits — won’t repeat.

Absent such catalysts in 2026, automakers face a choice: constrain production to protect pricing power and profits or employ higher incentives that drive demand but reduce margins and risk ballooning inventory.

For dealers, the better scenario is clear. New-vehicle pricing and profit dynamics erode when industry sales exceed 16 million units annually. But even if automakers go the volume-pushing route, retailers fortunately have other levers to pull to maintain operational discipline and profitability.

Those other avenues, which typically generate better margins than the new-vehicle business, include:

- Parts, service and warranty, a high-margin business with lots of demand created by an aging U.S. vehicle fleet

- Used-vehicle sales, poised to benefit from an improving pipeline of late-model and off-lease cars and trucks as the industry climbs out of a supply trough caused by pandemic-era production cuts

- Finance and insurance income, which is rising on a per-unit basis industrywide and helps dealers squeeze more profit from even low-margin vehicle sales

- Productivity gains from new or evolving technology tools as artificial intelligence software boosts dealership operating efficiency

New-vehicle segment under pressure but could produce more revenue and profit with less volume in 2026

New-vehicle volume gains appear unlikely against a 2025 that boasted the industry’s highest unit sales since 2019.

U.S. consumers rushed to buy last March and April ahead of expected tariff-driven price hikes, pushing the seasonally adjusted annual sales rate above 17 million for both months. That rate had previously not topped 17 million since April 2021. Federal EV tax credits expiring Sept. 30 then boosted SAAR above 16 million in all three months of the third quarter as automakers offered additional incentives to pare down EV inventory.

Without such catalysts in 2026, the big question is how manufacturers respond. If they are disciplined about production and align supply with demand below 16 million units, they and their retailers can stabilize profitability. While this is a rational and sustainable strategy, automakers may not follow it. After all, their market valuations tend to rise only when new-vehicle volume is growing.

Though overproducing drives volume, it is a poor option for manufacturers especially when rising costs — including the increased pass-through of tariffs to consumers — are likely to inflate vehicle prices, mute demand and further erode margins.

Automaker profitability will be more tenuous in 2026 as the market adjusts to a supply-demand balance that’s more organic than at any point since 2019, just before the onset of the coronavirus pandemic.

Operating leverage was important to earnings growth during the pandemic. Automakers and retailers cut costs in a low-interest-rate environment and then rode the wave of a measured production recovery below or in step with consumer demand from 2021 through 2025.

Supply-demand balance in 2026 will be much more at risk of tipping to oversupply. If manufacturers ramp output to drive 16 million-plus volume, automakers and dealers could end up with their worst pricing power and margin integrity since 2019.

Automakers have capacity to accelerate output. Vehicle production in North America dropped 4.3% year-over-year through November 2025 with some assembly disrupted by higher tariff-related costs. Higher-cost factories were hit harder, with U.S. output dipping 5.3% and Canada assemblies dropping 6.9% while Mexico’s builds rose 5.7%.

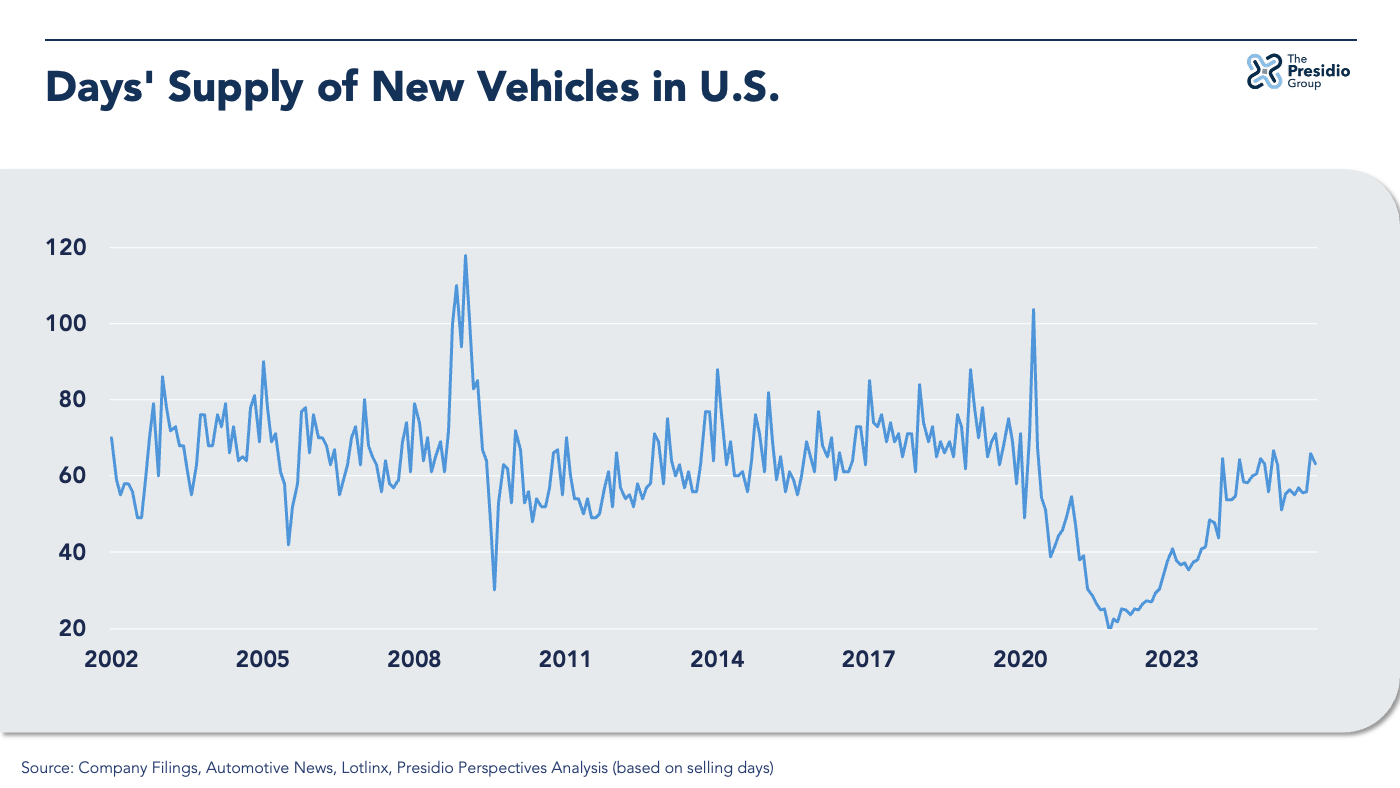

Given deteriorating demand in the U.S., increased production in 2026 would likely lead to a supply pile-up early in the year. If inventory rises much above its Dec. 1 level of 3.2 million units and a 63-day supply, automakers and dealers likely would have to respond with increased incentives and discounting, hurting their margins.

On the other hand, if 2026 volumes are lower, dealers won’t be able to sustain their approximately $800 billion new-vehicle retail revenue pool without higher average transaction prices. But consumers already are already showing signs of buckling under the pressure of high prices. Loan delinquencies above 30 days are already 3.9% of the total U.S. auto loan pool – their highest level since 2010 in the aftermath of the global financial crisis.

As cost of vehicle ownership continues to rise, consumers will struggle to afford increasingly expensive vehicles. The U.S. debt markets are expecting the Federal Reserve to provide some relief to the consumer by continuing to cut interest rates. But tension around future rate cuts persist. Increases in gross domestic product of 4.3% in the third quarter of 2025 and 3.8% in the second quarter are more indicative of an overheated economy for which rate increases are often employed to keep inflation in check.

The U.S. market is at a tipping point where price and profit could be traded for volume

Current U.S. new-vehicle supply resembles 2019 more than any year since. The industry sold 16.9 million vehicles that year, the fifth highest annual total in history, but automaker and dealership profitability was historically weak. Public dealership groups’ new-vehicle gross margin averaged 4.1% in 2019, its lowest performance since at least 2005.

Industry profitability ultimately hinges on striking the right balance of automaker-driven supply and consumer demand. Dealers commanded record price and profits when the coronavirus pandemic structurally altered the global automotive supply chain, slashing inventory and shifting the supply-demand balance sharply to the industry’s favor.

With that balance now closer to historic norms, the industry could soon be flirting with oversupply. U.S. sales have risen for three straight years from the pandemic’s low of 13.8 million new vehicles in 2022. While earnings have moderated with sales volume recovery, franchised dealers’ 2025 profits were on pace through three quarters to nearly double 2019’s levels, according to the Presidio-NCM Average Dealership Performance Benchmark.

But those higher profits to which dealers have become accustomed are at risk should overproduction push sales past 16 million new vehicles in 2026. Margin-compressing discounts from dealers and incentives from automakers would be necessary to move that much metal. New-vehicle gross profit already has slid sharply from its pandemic-enhanced peak of $4,772 in the first quarter of 2022 to $1,840 in 2025’s third quarter, according to the Presidio-NCM benchmark.

The industry finds equilibrium and sustainable profitability at annual new-vehicle sales of 16 million or fewer. Since 2012, U.S. new-vehicle sales have averaged 1.3 million units per month or 15.95 million annually. Inventory over that period averaged 3.0 million new vehicles, a 58-day supply when calculated on a selling-day basis. Today’s supply level already is above that historical average, starting December at 63 days.

At the current inventory count, monthly sales would have to average 1.43 million new vehicles to hit the 60-day supply level considered manageable for the industry. That’s 157,000 more vehicles than were sold in November. It’s a tough target: Monthly new-vehicle sales have topped that level less than a third of the time over the last 25 years. They hit that level during four months in 2025 — three because of the pre-tariff demand surge with the fourth related to the EV tax credit expiration.

If the industry can trim inventory by 385,000 vehicles and keep stock levels below 2.7 million units, automakers and retailers would be better positioned to sustain profitability at the historical sales volume of 1.32 million vehicles per month since 2012.

But that may not be realistic given the pressure automakers are under to improve capacity utilization of their assembly plants. An 80% utilization rate is ideal. U.S. automotive assembly plants have run below that threshold for 32 consecutive quarters. They’ve operated below 70% for the last eight quarters.

It puts automakers in the position of running factories well beyond the level of production aligned with organic consumer demand in search of economies of scale and revenue to absorb their fixed costs. While overproducing and then creating demand with retail discounts and factory incentives typically drive volume growth, it damages the profit dynamic of the industry in the long run.

Revised EV strategy will likely shift profit mix even more to high-margin trucks

Off-lease supply in 2026 will post the first increase since 2022 as full-line dealers diversify revenue to other business units in response to muted new vehicle sales as prices continue to inflate. As a form of factory incentive to drive demand, leasing accounted for 31.1% of the 16.9 million new vehicle transactions in 2019, driving 2022 lease returns – the average lease term was 36 months in 2019 – to 5.3 million. The supply chain disruption during the COVID-19 pandemic muted supply so much that consumers paid over MSRP and automakers eliminated incentives. In 2022, total new vehicle unit sales were 13.8 million and lease penetration was 17.5% and while it was the most profitable year in history for the franchised dealer base, it starved the used vehicle market of supply in 2025.With the expiration of the EV tax credit, automakers are rethinking how electrification fits into a more organic selling environment. The entire U.S. automotive value chain, including franchised dealers, had been financially squeezed between government EV mandates and slow consumer adoption, resulting in persistently unfavorable profit dynamics. It will take automakers and retailers a long time to recover from their sunk costs in the EV space, and manufacturers will likely load 2026 with asset write-downs and one-time charges.

Automakers aren’t backing away entirely from EVs. But with consumers unwilling to pay profitable prices for the latest EV technology, automakers will be searching elsewhere to generate margin and grow earnings. Automakers can gain segment share with more affordable EVs while they manage the financial burden of the money-losing technology. The goal: Introduce the technology to entry-level and move-up to build a base for the future.

Without a lift from EVs and facing a potentially worse supply-demand imbalance, franchised dealers in 2026 will be looking for growth in other areas of the business like used-vehicle sales, parts and service and finance and insurance. And even if new-vehicle margins get squeezed further, dealers can still use those low-profit sales to expand F&I income and create new service customers.

Supply tail wind will provide used-vehicle growth opportunities

The number of vehicles coming off lease will rise in 2026 for the first time since 2022.

Prior to pandemic-related production shortfalls, automakers commonly incentivized leases to drive demand. Leasing accounted for 31.1% of 2019’s 16.9 million new-vehicle sales, fueling lease returns of 5.3 million units in 2022. But automakers largely eliminated leasing incentives after the pandemic’s supply chain disruptions lowered inventory. Lease penetration dropped to 17.5% by 2022 when new-vehicle sales totaled 13.8 million. While that became the most profitable year in history for franchised dealers, it meant many fewer vehicles coming off lease to stock used-vehicle lots in 2025.

Dealers are still profiting from that scarcity. Through the first three quarters of 2025, the public dealership groups increased their used-vehicle gross profit pool by 10% even though revenue rose by only 0.7% and used-vehicle volume dropped 1.1%. On a per-unit basis, average revenue for the peer group grew 1.1%, while gross profit jumped 9.6%.

That dynamic will shift in 2026 when off-lease supply increases by 31.1%, or 750,000 vehicles. In 2027, off-lease supplies will rise by another 13.7%, or 433,000 vehicles. This marks the beginning of changing revenue and profit dynamics in the used-vehicle segment. With the aforementioned pressure on new-vehicle sales, franchised dealers are likely to increase their used-vehicle activity. Rising used volume would expand dealer revenue and gross profit pools, albeit on narrower margins as competition heats up. Even with off-lease supply gains, dealers will likely continue to pay more to acquire used inventory than pre-pandemic.

Franchised dealers continue to deploy more attention and resources to fixed ops

With— and at an increasing average age with more miles driven — dealers’ repair and maintenance business will grow even as competition for that revenue intensifies.

With new-vehicle profitability under pressure, dealers already are putting more focus and resources into their fixed operations to leverage the latter department’s superior profit dynamics. That will continue even as operators carefully monitor the capacity utilization of their parts and service facilities and already-constrained technician workforce to maximize their use for higher-margin work.

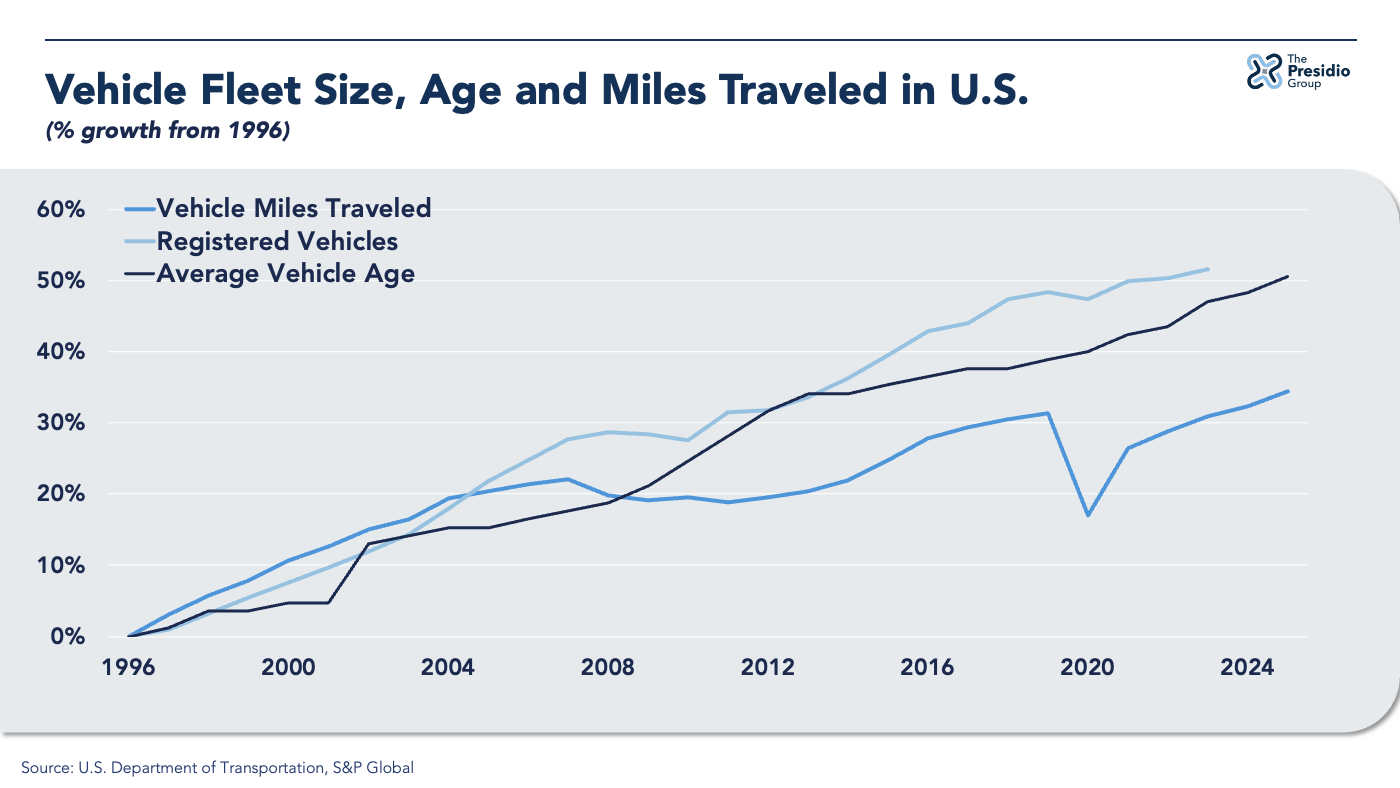

The average U.S. vehicle age is now a record 12.8 years. With vehicle reliability critical to customer loyalty, automakers must continuously improve their build quality, parts availability and repair and maintenance processes. That means the U.S. vehicle fleet will continue to age and drive more auto care business to dealerships.

The size of the registered fleet will continue to expand. The U.S. had 306 million registered vehicles in 2023 compared with 197,000 in 1996. Automakers have kept production well above scrappage rates in most years, consistently increasing the size of that fleet.

Vehicle miles traveled in the U.S. were 3.28 trillion in 2024, surpassing the previous record of 3.26 trillion miles in 2019. The country is on pace to set a new peak of 3.34 trillion in 2025. The combination of the largest registered fleet in U.S. history, the oldest average vehicle age and the most miles driven should deliver an expanding repair and maintenance revenue pool for franchised dealers.

Basic repair and maintenance services are a tough sell as dealership labor rate climbs

With the technician shortage and increasing costs moving effective labor rates higher, dealerships may continue to lose low-margin business to independent repair shops, oil change chains and mobile service companies. Dealerships handled 12% fewer service visits in 2025 compared with 2018, according to a study by Cox Automotive. Some of that lost business, however, may carry narrow margins or represent work that’s been upsold into a larger service visit requiring more hours but reducing the repair order count.

Performing basic maintenance can create repeat customers and feed new- and used-vehicle purchases over the long term. But escalating costs for real estate, tools, technology and labor makes that low-margin business less attractive, especially to a service department with capacity constraints. When franchised dealerships use technology and proprietary diagnostic tools to increase the hours and labor rate per job, they can still grow revenue and profits even if repair orders are shrinking.

A Reynolds and Reynolds study found that the largest dealerships using automated tools to quote customer-pay work averaged $56,508 more profit per month than those that don’t. That equates to an additional $678,096 in profit annually. Dealerships at the industry’s median number of repair orders generate an additional $9,345 in monthly profit using automated quoting tools, or $112,140 annually, Reynolds found.

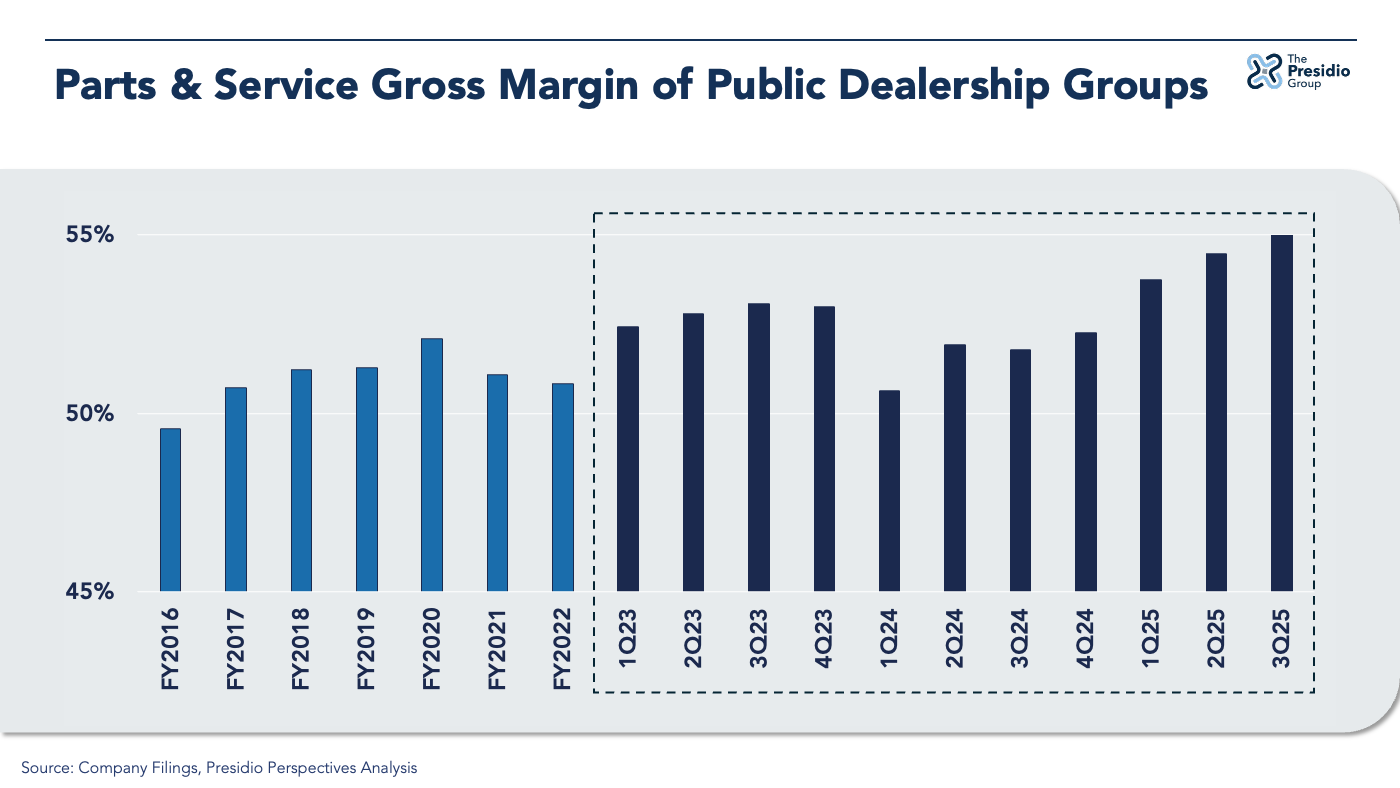

Public dealership groups have consistently improved their parts and service gross margins. The six public groups grew that margin by 378 basis points on average to 54.4% through the first nine months of 2025 and also raised revenue by 7.2%. Gross profit for the group was on a $10.5 billion run rate for the full year, or approximately $6.3 million in fixed ops gross profit per franchise.

New technology from vendors is creating more operating efficiencies for dealers

With gross margins under pressure, retailers are looking for ways to wring out additional profit through efficiency and productivity gains and cost controls across their operating lines.

Even as new-vehicle margins shrink, dealerships’ other three main business units — used vehicles, fixed ops and F&I — have more opportunities to boost profitability, as demonstrated by gains for those departments for the public dealership groups through the first nine months of 2025.

Improving gross margin, however, is tough when competitors have similar strategies, and the economic climate makes consumers wary to spend. It behooves dealers to look beyond the normal channels to reduce costs and increase productivity. With artificial intelligence taking a larger role in all aspects of automotive retail, it is likely that low-margin tasks will be passed off to software systems that can organize, schedule, track and reorder while human resources focus on relationship building, growth prospects and more complex tasks.

AI tools and tech platforms that help dealerships sell and service more vehicles are plentiful and evolving. Dealers already have expanded their use of such tools and are expected to continue experimenting with them in 2026.

Revenue diversity will be key for dealerships in 2026

With new-vehicle gross margin likely to continue to contract in 2026 — the publics’ recent 6.2% average in that category was the peer group’s lowest such mark since the third quarter of 2019 — dealers have to look elsewhere. Their other business units are the obvious answer.

With 2026 poised to deliver the industry’s first period of organic supply and demand since 2019, retailers have a clear view of their opportunities and challenges for the near and intermediate term. With a diversity of revenue that their automaker partners lack, franchised dealers should be able to cycle resources to their best-earning business units. It means 2026 is shaping up to be a pivotal year for retail automotive.