The six U.S. public dealership groups entered 2026 facing a less forgiving operating environment. As vehicle margins continued their retreat from pandemic-era highs, sales volumes softened against a tough year-ago comparison with affordability pressures, geopolitical conflict and economic uncertainty weighing on consumer demand. Earnings slipped for five of the six public groups in the first quarter of 2026 as their operating costs rose, consuming a larger share of gross profit.

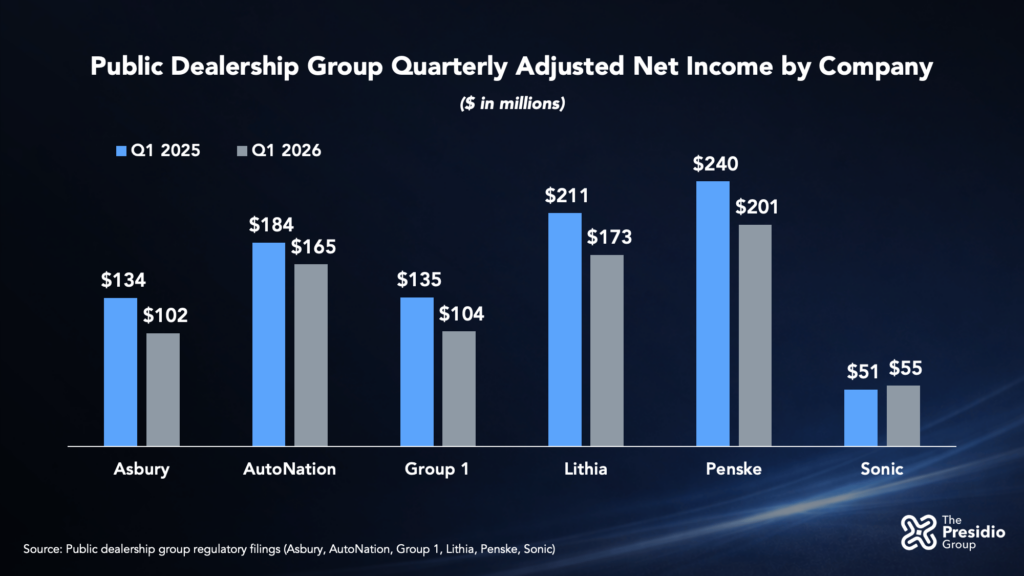

Collectively, the public groups — Asbury Automotive Group Inc., AutoNation Inc., Group 1 Automotive Inc., Lithia Motors Inc., Penske Automotive Group Inc. and Sonic Automotive Inc. — generated $800 million in adjusted net income in the first quarter, down 16.2% from the comparable period in 2025. Only Sonic posted a profit increase.

The industry was up against an unusually strong prior-year quarter from a new-vehicle volume and margin perspective. In March 2025, consumers rushed to buy vehicles ahead of expected U.S. tariff hikes, boosting sales and new-vehicle profitability across the industry.

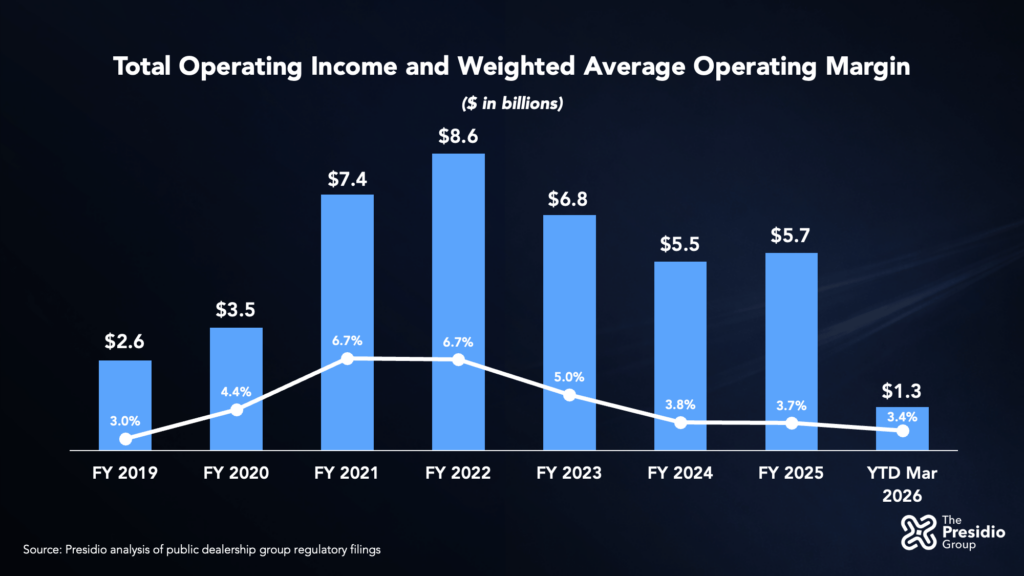

The first-quarter decline underscores how much the profit equation has shifted for dealers. With operating margins across the public peer group well below the peak years of 2021 and 2022, public group executives in their first-quarter earnings emphasized the importance of higher-margin businesses such as parts and services. They also stressed the need to tighten their expenses and framed some store divestitures taken in the quarter as moves to protect returns and capitalize on strong dealership valuations.

Vehicle margins continued to retreat

As the industry worked through payback from the demand pull-forward of early 2025, new-vehicle margins continued to fall. Using Presidio’s weighted U.S.-adjusted peer composite, which excludes non-franchised dealership and non-U.S. operations where possible, same-store gross profit per vehicle for the public peer group fell 6.8% to $3,253. Adjusted same-store new-vehicle unit sales dropped 9.0%.

The combination of that volume decline with lower margins meant adjusted same-store new-vehicle gross profit dollars tumbled by double-digit percentages for all six public dealership groups, with year-over-year declines for each company ranging from about 12% to just over 20%.

Executives signaled a more pragmatic approach to the new-vehicle business.

“I’m comfortable with margin mitigation because I think it will translate into volume,” said AutoNation CEO Mike Manley. “I do think that there is a large amount of pent-up demand now in new. It’s also translated into used to some extent.”

Used-vehicle results were also down for the publics but to a lesser degree than on the new side. Using Presidio’s U.S.-adjusted peer composite, same-store gross profit per used vehicle retailed declined 2.5% for the peer group to $1,743. Adjusted same-store used retail volume dropped 2.5% on a composite basis. That combination of lower volume and margin resulted in declines in total used-vehicle gross profit dollars for each of the six companies that ranged from nearly flat to down about 11%.

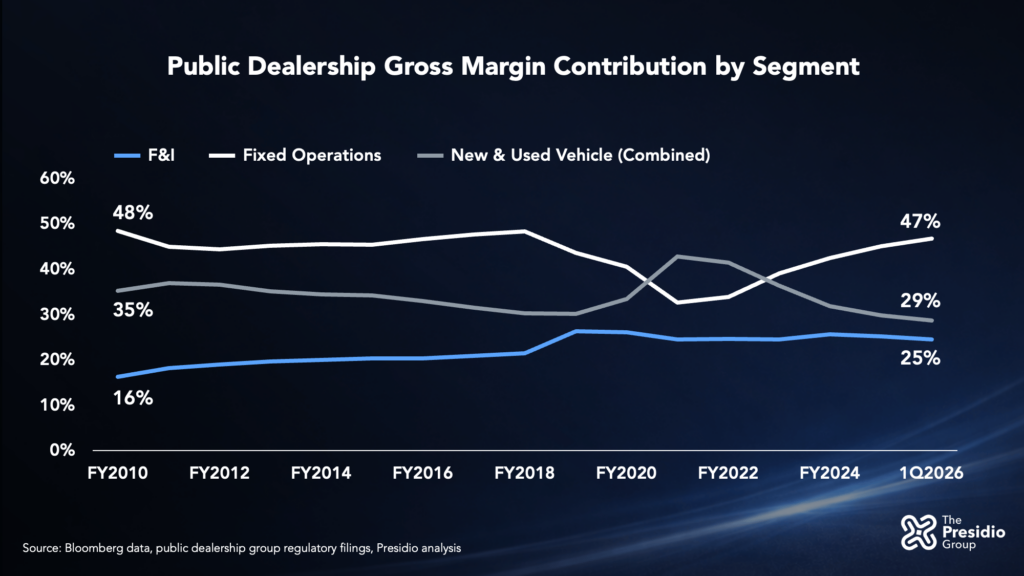

Fixed operations carry profits

Higher-margin business lines continue to help soften the earnings impact from the weaker vehicle sales environment.

Finance and insurance remains a critical profit contributor, helping offset weaker front-end results in the first quarter as new-vehicle sales and margins normalized. Using Presidio’s U.S.-adjusted peer composite, same-store F&I gross profit rose 2.0% to $2,193 per vehicle.

And public group executives consistently highlighted their parts-and-service results for the first quarter. This fixed-operations business line has become central to earnings across the public groups, reflecting both its higher profit level, recurring nature and importance as a driver of customer engagement and retention.

Using a Bloomberg weighted composite analysis, fixed operations accounted for 46.8% of total gross profit for the peer group in the first quarter.

Several companies cited record fixed-ops results. Penske said it posted record first-quarter revenue and gross profits from its parts-and-service business. AutoNation reported a first-quarter record in fixed-operations gross profit. Group 1 said its parts-and-service gross margin in the U.S. reached a quarterly high.

Sonic said it set quarterly gross profit records in both F&I and fixed operations.

“These two high-margin business lines continue to increase their share of our total gross profit pool, once again contributing over 75% of total gross profit for the first quarter, mitigating the potential headwinds to new-vehicle volume and margin to our overall profitability,” Sonic CEO David Smith said.

Expenses increase, forcing cuts

As gross profit declined in the first quarter, operating costs consumed a larger share of gross across the public dealership groups, sharpening management focus on expense control.

On a weighted composite basis, adjusted selling, general and administrative expenses accounted for 71.6% of total gross profit in the quarter for the publics, up from 68.5% in the year-earlier quarter. That deteriorating operating leverage had several companies making moves to target cost cuts.

Group 1 announced it initiated cuts in its U.S. business in early April after first-quarter SG&A performance in the market failed to meet expectations. Headcount was trimmed by nearly 700 full-time employees. That along with contract and vendor elimination was expected to reduce $50 million in annual costs and return SG&A leverage “to a more acceptable level,” CEO Daryl Kenningham said.

“We continue to look for ways to leverage technology, including artificial intelligence, to improve our returns,” Kenningham added.

AutoNation reported that operating costs ran above its long-term target range during the quarter, citing marketing spending and weather-related impacts. AutoNation executives said costs should ease later in the year. Lithia also pointed to actions in its sales departments to reduce expenses, namely tightening variable compensation and better alignment of staffing.

Across earnings calls, the message was blunt: Cost structures built for higher volumes are being pared back to fit a weaker vehicle volume and margin environment.

Technology is one avenue to improved efficiency anticipated by public group leaders. Asbury and Lithia both provided updates on their rollouts of new dealership management systems. Asbury had converted more than half of its stores to Tekion’s DMS by the end of the first quarter. Outgoing CEO David Hult said the transition has created short-term disruption but is necessary to improve long-term efficiency.

Lithia said its rollout to Pinewood.AI’s tech tools, including its DMS, is aimed at simplifying store processes and reducing long-term operating costs, even though benefits are expected to accrue gradually. Lithia CEO Bryan DeBoer has said the move will reduce annual tech costs, once estimated at $100 million, by up to $40 million.

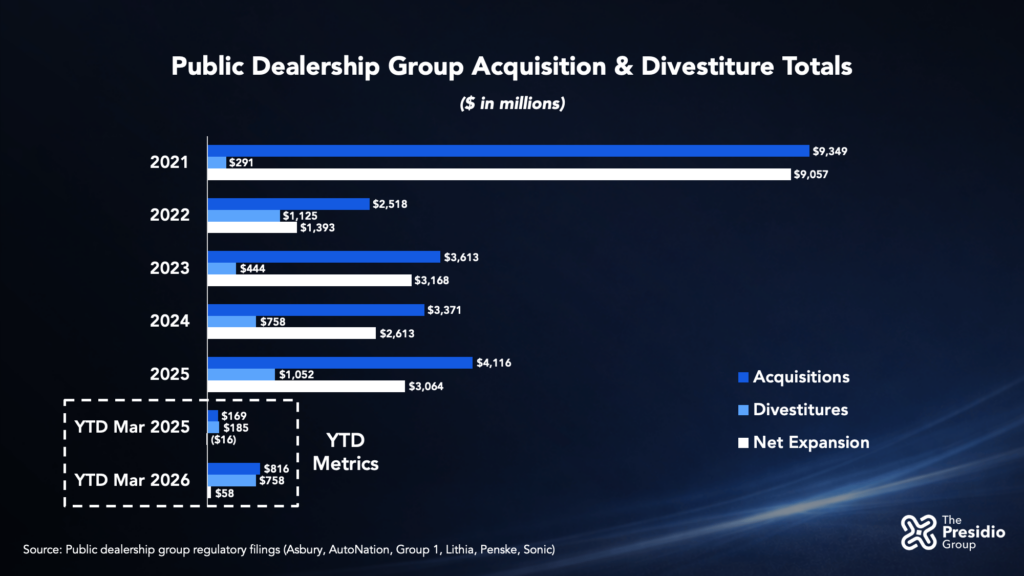

Reshaping dealership networks through active portfolio management

Dealership acquisitions and divestitures played a more uneven role across the companies in the first quarter. Apart from Lithia and Penske, acquisition activity across the peer group slowed during the quarter, even as the broader dealership buy-sell market recorded a year-over-year increase in transactions for the period.

Penske spent $670 million on acquisitions in the first quarter, the most of any public group. It bought two large-scale Lexus dealerships in the Orlando, Fla., market that are expected to add $450 million in annual revenue. Penske also divested a Rhode Island Lexus store in March. CEO Roger Penske in April described Penske’s M&A strategy in part as shedding low-performing stores and acquiring key dealerships that can deliver the kind of returns the company is targeting.

“So we’ll continue to prune the portfolio,” Penske said. But “we’re still in the acquisition business.”

Several publics leaned more on divestitures in the first quarter. Proceeds from store sales rose for much of the peer group, with Asbury and Group 1 emerging as the most active sellers.

Asbury CEO David Hult framed the company’s elevated divestiture activity as a deliberate capital-allocation decision positioning the company for future success.

“We divested 10 dealerships and a collision center at attractive multiples, representing approximately $600 million in annualized revenue,” Hult said.

At Group 1 Automotive, CEO Daryl Kenningham pointed to cost structure and capital demands behind the stores sold during the quarter.

“We divested two Mercedes-Benz dealerships in California. These stores were high-cost operations with significant real estate and operating constraints,” Kenningham said.

Presidio advised Group 1 on its sale of Mercedes‑Benz of Beverly Hills in March and Asbury on its sales of the Plaza Motors platform in St. Louis and three dealerships in Greenville, S.C., in February.

Those publics’ divestitures reflect a growing trend toward active portfolio management among the industry’s largest dealership groups. Many large public and private operators are selling stores tied to certain brands or exiting less strategic markets and redeploying capital into dealerships that better complement their existing or target footprints and align with their long-term strategic objectives.

Despite the slower pace of acquisitions in the first quarter, the public dealership groups continue to have substantial financial capacity to do deals. As of March 2026, the peer group held $7.3 billion in total liquidity, down from $7.6 billion at year-end 2025 but still 80% higher than pre-pandemic liquidity levels.

That leaves the publics flexibility to remain selective while retaining the capacity to execute on desirable acquisition opportunities that become available in the market.

Bottom line: The first quarter of 2026 clarified the tougher vehicle-sales environment facing public dealership groups. Vehicle margins are lower. Fixed operations are accounting for a larger share of profits. Operating costs have become harder to absorb. Management teams are responding with moves to better control expenses. It means results will be increasingly shaped by cost control, fixed-operations execution and disciplined portfolio decisions as dealership groups adjust to a less forgiving retail landscape.