Full-line franchised dealerships will find it challenging to build an ample used-vehicle inventory with strong profit potential given that the flow of late-model, low-mileage used vehicles coming off lease will be sparse through 2027. Historically low new-vehicle production combined with meager lease penetration through the pandemic period of 2020 through 2024 will leave retailers undersupplied with used cars and trucks for the next several years. As dealers seek to diversify their revenue generation because of compressing new-vehicle margins, they will have to put a greater focus on fixed operations to take up the profit slack while waiting for the supply dynamics of the used segment to improve.

New-vehicle volume dip during pandemic creates undersupplied used-vehicle segment

The primary driver of used-vehicle scarcity in the U.S. was the significant slowdown in production and sales of new cars and trucks beginning in 2020. In the five years immediately prior to the pandemic, new-vehicle volume in the U.S totaled 86.7 million units, or an average of 17.3 million vehicles per year. Full-year 2019 sales of 17.1 million vehicles marked the fifth straight year of sales above 17 million after the industry climbed back from a 27-year low of 10.4 million vehicles in 2009 during the global financial crisis. By contrast, U.S. new-vehicle unit sales from 2020 through 2024 totaled 75.1 million, an average of 15 million vehicles annually and 13% lower than the five-year total before the pandemic.

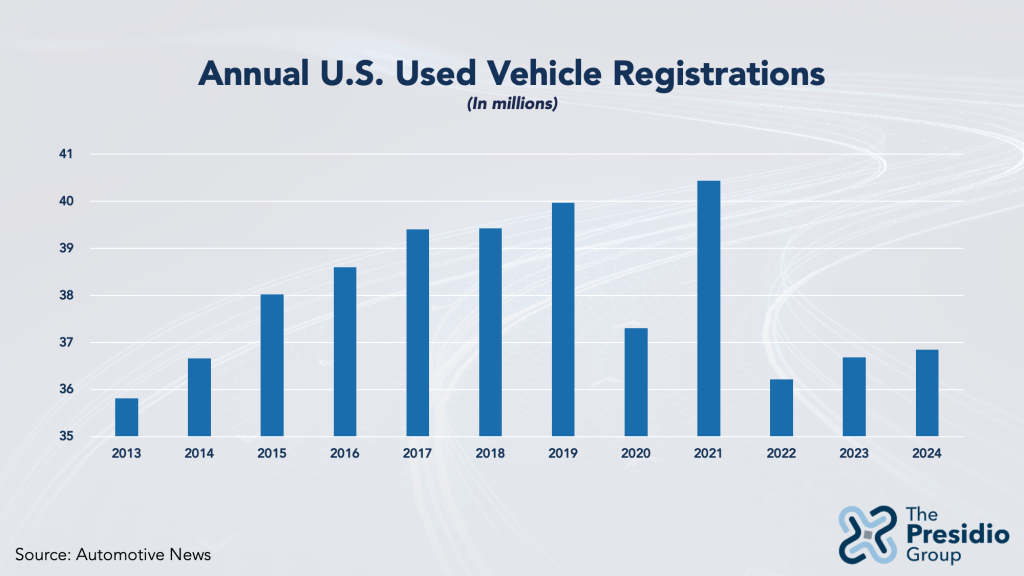

The tighter supply and demand dynamics of the new-vehicle segment essentially eliminated factory incentives in 2021 and 2022 and created a firm and elevated pricing environment. Consumers reacted to expensive new vehicles by migrating to the used segment, well stocked by high leasing volume in the 2015-19 period. Those dynamics led to record used volume in 2021 that topped 40.4 million transactions. But sales fell 10.4% in 2022 for a myriad of reasons — higher prices, rising interest rates and the beginning effects of lower availability of late-model vehicles caused by production interruptions. Consumers also were potentially able to defer purchases as U.S. vehicles in operation lasted longer given the lower mileage driven during the pandemic. Used volume recovered only modestly in 2023 and 2024 as the market grappled with undersupply even as automakers resumed more aggressive production.

Leasing idled during pandemic period of tight supply and demand balance as incentives were unnecessary

The unprecedentedly tight new-vehicle supply of 2020 through 2023 eliminated automakers’ dependence on factory incentives and leasing to manage inventory. During the record volume period of 2015-2019, 26 million new vehicles, about 30.2% of new volume, were leased. Considering the average U.S. lease term of 36 months, the used market had been underpinned by an annual off-lease flow of 5.2 million units coming back to market from 2018 through 2022. But from 2020 through 2024, leasing represented just 22.8% of total volume, creating a lease return shortfall of 11.7 million vehicles for 2023-2027 compared with the well-stocked 2018-22 period. Average annual lease returns will bottom out at an estimated 2.4 million vehicles in 2025 before rebounding to an estimated 3.2 million units in 2026 and 3.6 million in 2027. That still-significant dearth of used units is likely to keep pricing firm and elevated for retailers and consumers.

Lease returns, which historically average approximately 10% of total used transactions annually, are especially important to franchised dealers as a source of the highest quality late-model and low-mileage used vehicles potentially carrying the highest margins. While any dealer can provide a form of extended service protections to used-vehicle buyers, the off-lease supply typically is the source of certified pre-owned vehicles for which only same-brand franchised dealerships can offer extended factory backing.

Full-line franchised dealerships may not soon find relief from inflated wholesale prices as they must also compete with pure-play used-only retailers such as CarMax and Carvana for the narrower supply of units. Both CarMax and Carvana generate more than 90% of their revenue from used-vehicle sales — both retail and wholesale – and are intent on securing inventory to supply their core businesses and earnings generation engines. CarMax sold 1.3 million units in 2024, more than double any other competitor, while Carvana topped 616,000 units. Full-line dealerships may be in the crossfire of inventory acquisition between those two used-only giants, meaning the competitive landscape could lead to overpaying for vehicles to keep showrooms and websites stocked.

As full-line dealerships look to offset compressing new-vehicle margins with a greater focus on other business units, the franchised peer group will be navigating tight used-vehicle supply and inventory-hungry competitors in CarMax and Carvana. The conditions of the used-vehicle segment should support firm pricing and margin integrity, though desperation to keep lots stocked may shave off some level of profitability as dealers compete and potentially overpay for quality used units.