The rate of profit decline for the U.S. franchised dealer base has slowed and may stabilize in 2025. Still, risk remains that manufacturers’ efforts to utilize their excess production capacity — even if the resulting supply lacks organic consumer demand — will create toxic unit volume growth in the U.S. that is likely to trigger further margin compression.

The six publicly traded dealership groups’ combined adjusted 2024 earnings before interest, taxes and depreciation (“Ebitda”) of $7.7 billion was the peer group’s lowest level since 2021 and marked the second consecutive year-over-year decline in the total since the global financial crisis devastated the industry in 2009. The inverse relationship of higher profit on lower volume was evident in 2021 and 2022 as the group’s adjusted Ebitda crested $8 billion in both years, even as the industry’s total new-vehicle sales dipped in 2022 to 13.9 million units, its lowest total since 2011.

Automakers may not be exhibiting enough production restraint as the total number of vehicles assembled in North America increased 2.8% in 2024, running ahead of the 2.3% gain in unit sales for the year. That kind of imbalance creates concern that inventory could balloon enough to hurt the industry’s pricing power and require discounting that would shrink gross margin for both manufacturers and dealers. New-vehicle inventory at the end of 2024 was 25.5% higher than at the end of 2023, translating to 12 additional days of supply based on the fourth-quarter selling pace. New-vehicle production in the U.S. rose 4.5% last year, while Canadian output declined 11.3% and Mexican production increased 3.1%.

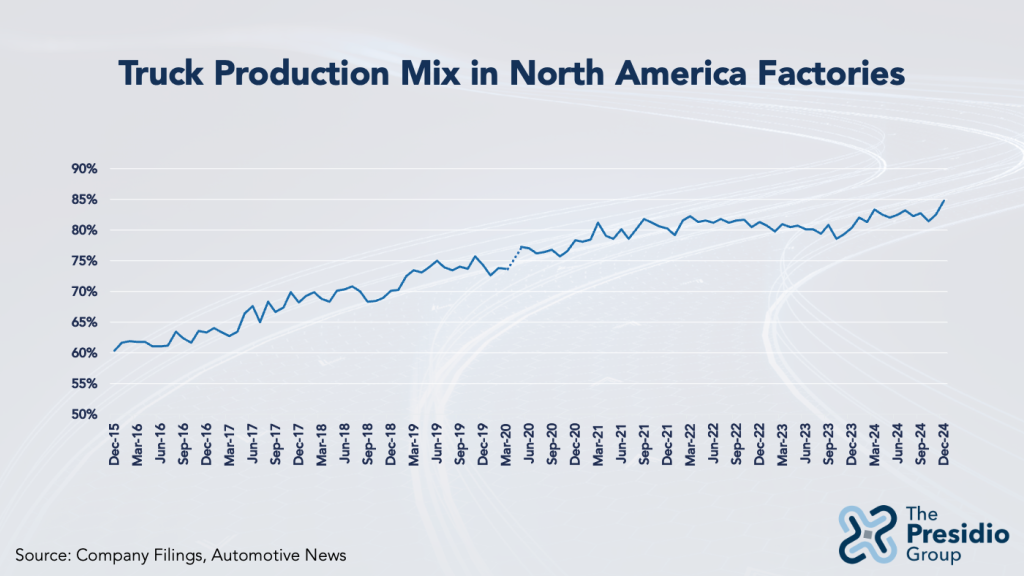

North America’s production mix by body type presented a more noteworthy change: Car output fell 9.5% and represented only 17.5% of total builds, the lowest level on record. Light truck production increased 5.9%, indicating that mix will continue to be dominated by higher-priced vehicles that drive per-vehicle profit contribution. Trucks represented 84.7% of North American production in December and 82.1% of the retail sales mix — both record highs. Little additional upside to this profit-rich vehicle mix may exist, creating concern that automakers could face a financial dilemma as prices and margins flatten — at least until the industry’s next profit catalyst is identified and pursued.

Production Cost Inflation Forces Automakers to Put the Pedal Down on Output

Rising costs, from raw materials to labor, put automakers in a corner, leading them to maintain capacity and produce at levels that increasingly exceed demand. The resulting crimp in profit margins is felt throughout the automotive value chain. The current inventory level of around 3 million vehicles is more than twice average monthly unit sales in the market and is drifting toward pre-pandemic peaks that regularly reached 4 million vehicles. As inventory creeps up, manufacturers and retailers will surrender pricing power and margin integrity, further building the case to for automakers tackle capacity and costs cutting.

Ford and General Motors have wrestled with rising supply and production costs even as they’ve reduced their global manufacturing footprints and retrenched production in North America. GM’s cost of goods sold per vehicle has increased 122.4% since 2015 to $25,173 in 2024. Ford’s per-vehicle bill of goods grew 90.9% during the same period, to $37,916 last year. Inflated per-vehicle production cost is also a function of more expense spread over fewer units of output. Since 2015, GM’s global production plunged 39.9% to 6 million vehicles. Meanwhile, Ford has built fewer than 4.5 million vehicles globally every year since 2019, down from a peak of 6.6 million in 2016.

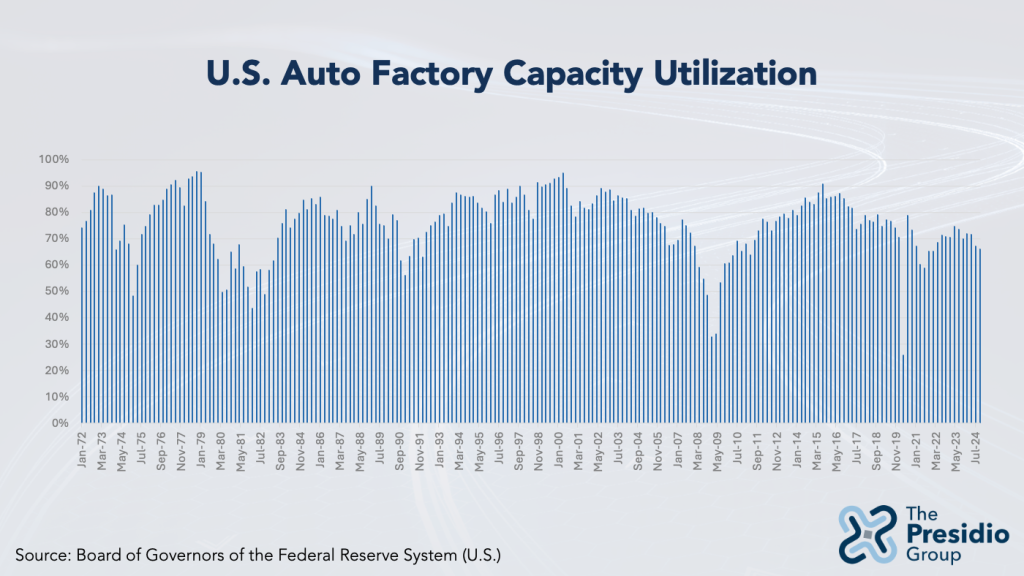

Reining in output, however, does not appear to be an immediate priority. Supply-chain analysis company JustAuto forecasts there will be 24.5 million units of total new-vehicle assembly capacity in North America by 2028 but only 16.4 million actual builds — a 67% utilization rate. Automotive factories target 80% as ideal. In the U.S., the actual utilization rate has been below that level for 30 consecutive quarters, the second worst stretch since 1972. The most disastrous period spanned 34 quarters from mid-2005 through mid-2013 and included the bankruptcies of General Motors, then-Chrysler Group and dozens of suppliers.

In the near term, retailers have a volume opportunity as automakers are increasingly under pressure to maintain elevated production levels despite a lack of corresponding organic demand environment. It likely will require more incentives and discounts to keep the metal moving. A macroeconomic or geopolitical shock, however, could disrupt the tenuous balance and force manufacturers to make structural changes that would have implications throughout the automotive value chain.