Auto dealers are increasingly concerned about the lack of available lower-priced, entry-level new vehicles in the U.S. market, amplifying an affordability outcry from consumers. But the growing lament is rooted in a misleading view of how affordability is measured in today’s market — and likely won’t substantially change automakers’ course as they plan their next generation of new vehicles.

Automakers have both little incentive and limited ability to restore the kind of broad-based new-vehicle supply considered affordable by the masses. After largely curbing the industry’s long-standing overproduction problem and concentrating on higher-margin products, the manufacturers have no will to unwind those moves for a fuzzy and moving target of affordability that comes at the expense of profitability.

Rising material, labor, regulatory and distribution costs make lower-priced vehicles difficult for automakers to produce at breakeven or modestly profitable price points. While Asian manufacturers with their lower cost structures generally still offer more nameplates below the industry’s average price than competitors, others such as the domestic brands from Ford Motor Co., General Motors and Stellantis couldn’t compete profitably in entry-level segments. They have exited that part of the market for clear financial reasons, prioritizing profitability over volume and market share.

Still, some OEMs are now planning lower-priced models in response to dealer and consumer pressure. Stellantis said in late May it would introduce nine vehicles priced under $40,000 in North America by 2030, including two below $30,000. GM reportedly is planning a new Buick sedan. And Ford is planning five models priced under $40,000 by decade’s end, including a $30,000 electric pickup.

But while automakers may revive some budget-friendly models, a return to broad-based entry-level pricing across their lineups is not realistic. That means franchised dealerships will likely continue to operate in a structurally weaker new-vehicle volume environment.

Even with fewer new-vehicle sales, dealers have a clear playbook — from shifting growth toward higher-margin business lines such as fixed operations to driving efficiencies across the store. Their opportunity is less about waiting for cheaper new vehicles and more about optimizing their own business line mix, expense structures and profit streams.

New vehicles are less expensive today adjusted for inflation and mix

The industry’s affordability debate is built on a fundamentally flawed premise, with an outsized focus on headline new-vehicle transaction prices, which have averaged close to $50,000 in recent months.

New vehicles indeed cost more just looking at the industry’s average transaction price. But adjusting for both inflation and, critically, the U.S. market’s shift toward higher-priced light trucks changes the picture: today’s vehicles are larger and more content-rich. They also require less of the average U.S. household’s income to purchase — the average transaction price represented 56.4% of household income in 2025 vs. 58.1% in 2016.

So while it is true that consumers are paying more in raw dollars, they’re also getting more, and automakers’ cost and margin pressures remain.

The average U.S. new-vehicle transaction price has risen 41.7% since 2016, breaking $49,000 for six of the last eight months. Over a longer horizon, the U.S. new-vehicle ATP has set records for 21 of the last 23 years. And today’s near-$50,000 mark is no doubt a psychological barrier for many consumers.

But that number looks much different when adjusted for inflation and, critically, vehicle mix. Through that lens, consumers are paying less than they did back in 2016 when the U.S. market set a volume record of 17.5 million new vehicles sold.

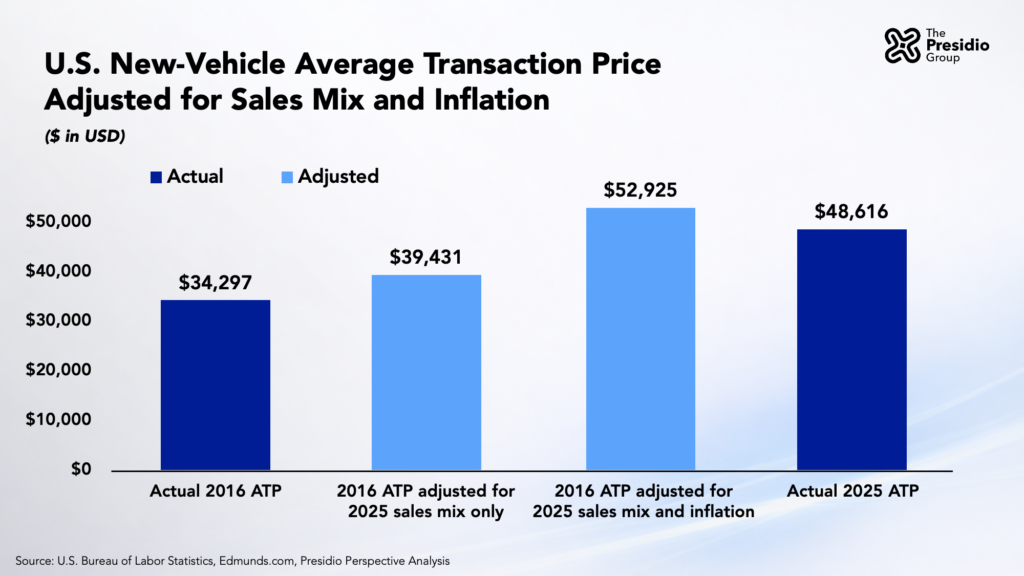

Adjusted for inflation alone, 2016’s average price of $34,297 translates to $46,038 in 2025 dollars — or 5.6% below 2025’s actual average of $48,616.

When the U.S. market’s shift toward higher-priced light trucks is incorporated, the comparison changes meaningfully.

Light trucks accounted for 60.6% of all U.S. light-vehicle sales in 2016, with an average price of $41,721 across pickups, SUVs, crossovers and minivans. Truck mix rose to 83.2% of all sales in 2025 at an average price of $49,897.

Holding prices constant and applying 2025’s mix to 2016 increases the average transaction price by 15%, or $5,134 per vehicle, to $39,431. Adding that mix adjustment to the inflation-only calculation pushes 2016’s ATP to $52,925 in 2025 dollars — more than last year’s actual average price.

This analysis shows that today’s larger, more content-rich vehicles are actually less expensive in real terms than in 2016.

Even so, higher interest rates and higher nominal transaction prices mean many consumers still feel meaningful payment strain, with many car buyers relying on longer loan terms to achieve a more affordable monthly payment.

Domestic brands struggle to keep pace on affordability

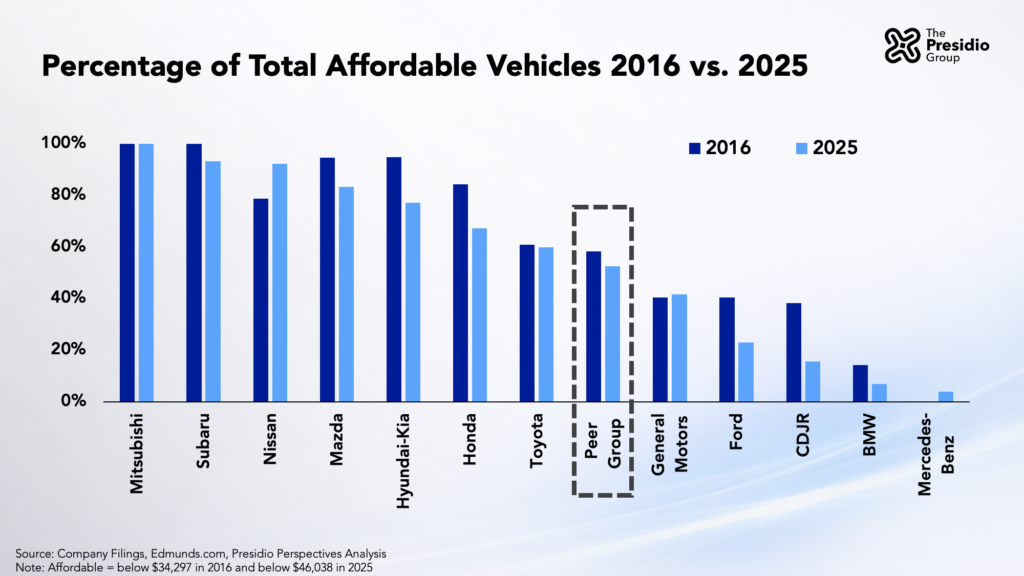

The industry’s mix of affordably priced new vehicles has fallen over time, with the steepest drops concentrated among domestic-brand automakers. In 2016, 49.4% of U.S. new-vehicle sales transacted below that year’s average price of $34,297, the benchmark used as a proxy for affordability in Presidio’s analysis.

By contrast, in 2025, 47.9% of sales fell below the industry’s inflation-adjusted average of $46,038, the comparable affordability benchmark for that year. When that benchmark is further adjusted to include the market’s mix shift toward higher-priced light trucks, the implied average transaction price rises to $52,925, with 57.2% of all new vehicles transacting below that level.

Over that period, brand-level shifts diverged sharply. Stellantis’ Chrysler-Dodge-Jeep-Ram collection of brands saw the biggest pullback in affordable mix, followed by Hyundai-Kia, Ford and Honda.

The Chrysler-Dodge-Jeep-Ram mix tumbled from 38.1% in 2016 to 15.6% in 2025 — a nearly 22.5-point decline. That reflected the automaker’s continued shift toward higher-priced pickup and SUV segments and its near exit from lower-priced passenger car segments, leaving the brands little room for offset as pricing moved higher.

Hyundai-Kia also saw a meaningful pullback, with affordable mix declining from 94.8% in 2016 to 77.1% in 2025, a 17.7-point drop that largely reflects a steady move upmarket for the brands even as their overall lineups remain among the most affordable in the industry.

Ford’s affordable mix fell from 40.3% in 2016 to 22.9% in 2025, a 17.4-point decline as the brand discontinued almost all cars and shifted toward higher-priced crossovers, SUVs and its flagship F-series pickup.

Honda saw a similar decline, with its affordable mix falling from 84.3% in 2016 to 67.2% in 2025, a 17.1-point drop, slightly less than Ford’s decline.

Despite the similar magnitude of decline, the two brands remain in very different positions. Roughly two-thirds of Honda’s sales mix remains affordable, while Ford’s affordable mix has fallen to less than one-quarter.

Nissan stands out as a clear exception to the industry’s broader shift upmarket. While most automakers reduced their mix of affordable vehicles, Nissan increased its by 13.6 percentage points, rising from 78.6% in 2016 to 92.2% in 2025. That leaves Nissan far more heavily weighted toward entry-level and mid-priced vehicles than most peers, reflecting a different approach to balancing volume and profitability.

Cost discipline will reward dealers more than waiting on affordable vehicles

The average new-vehicle transaction price in the U.S. is approaching, and could soon eclipse, the $50,000 mark. While that threshold carries psychological weight, the reality is that new vehicles, when compared on an apples-to-apples basis, are not less affordable than they were in 2016.

For dealers, there isn’t a substantial upside in pushing automakers to add more lower-priced vehicles at scale. A meaningful boost in entry-level volume would only come from reversing the changes in the truck-focused product strategy now embedded across the supply chain. That is unlikely to happen in any sustained way.

Put simply: the more rewarding path for dealers is to improve their own cost efficiency, tighten inventory discipline and maximize growth in their higher-margin business lines. Those are levers within their control and offer more potential than waiting for an unlikely broad-based reset in vehicle pricing.