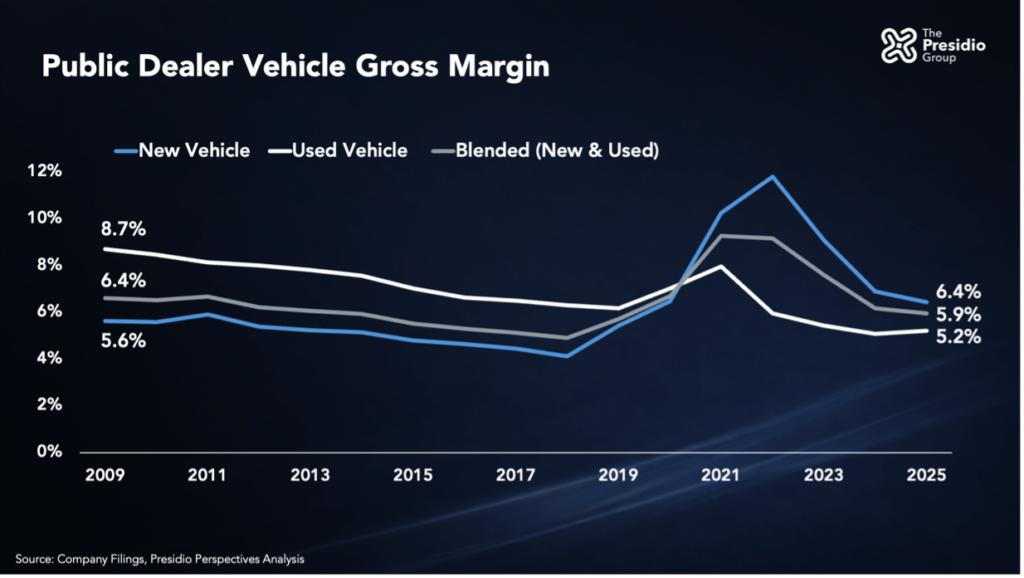

As vehicle margins continue to normalize, publicly traded dealership groups are driving revenue and gross profit growth in fixed operations and financial services — returning to a familiar earnings model that may matter more than ever. While peak new-vehicle profit margin of nearly 12% during the pandemic was a windfall for dealerships while it lasted, those splashy returns were a clear anomaly. Those gains also masked a decade-plus-long reality: compressing gross margins in both new and used vehicles.

For the publics, blended new-and-used gross margin fell every year from 2012 through 2018. When supply chain disruptions pared new-vehicle inventory by 75% during the COVID-19 pandemic, that blended margin jumped nearly 4.4 percentage points above 2018’s level, hitting a record 9.3% in 2021.

Used vehicles, historically more profitable than new, didn’t drive that gain. Since 2009, used-vehicle gross margin has shrunk by 3.5 percentage points, falling below 6% in each of the last four years. Average used margin dipped in 13 of the past 16 years. During the pandemic, new-vehicle margins surged above used-vehicle margins. While margin levels for the two operating lines have drawn closer as inventory constraints eased, they remain inverted compared with historical norms.

Moreover, it now appears margins for both new and used are resuming their pre-pandemic structural decline. That returns dealerships’ fixed operations and finance and insurance businesses to their role as primary profit drivers.

Inflation in gross profit dollars per new vehicle is offset by compressing margins

When gross profit dollars per new vehicle sold soared during the pandemic, dealerships enjoyed a windfall that briefly inflated the new-vehicle segment’s earnings contribution. But that was never going to last once supply constraints eased and production recovered.

New-vehicle transaction prices have stayed high even as dealership pricing power faded. From 2012 through 2025, the average U.S. new-vehicle transaction price increased 68%, or about 4.1% annually. Over the same period, public groups’ average gross profit per new vehicle soared 72.1% — a 4.3% compound annual growth rate — to $3,716. Inflation drove 41% of the gain, but mix mattered, too, as truck share rose 33 percentage points to 83.2% of U.S. new-vehicle sales by 2025.

But since the pandemic, higher prices haven’t consistently translated into wider margins. For the public peer group, new-vehicle gross margin declined by 5.4 percentage points from a peak of 11.8% in 2022 to 6.4% in 2025 even as transaction prices rose 4.6%.

Meanwhile, F&I gross profit per unit for the publics is up 93.3% since 2012, a 5.2% compound annual growth rate, outperforming both new and used with less volatility. Dealers have retained more of those gains, too. Per-vehicle F&I gross profit is down just 4.4%, or $101, from its 2022 peak of $2,280. By contrast, gross profit per new vehicle is down 37.5% from its 2022 peak of $5,950 for the public peer group, while used is down 29.2% from its 2021 apex of $2,479.

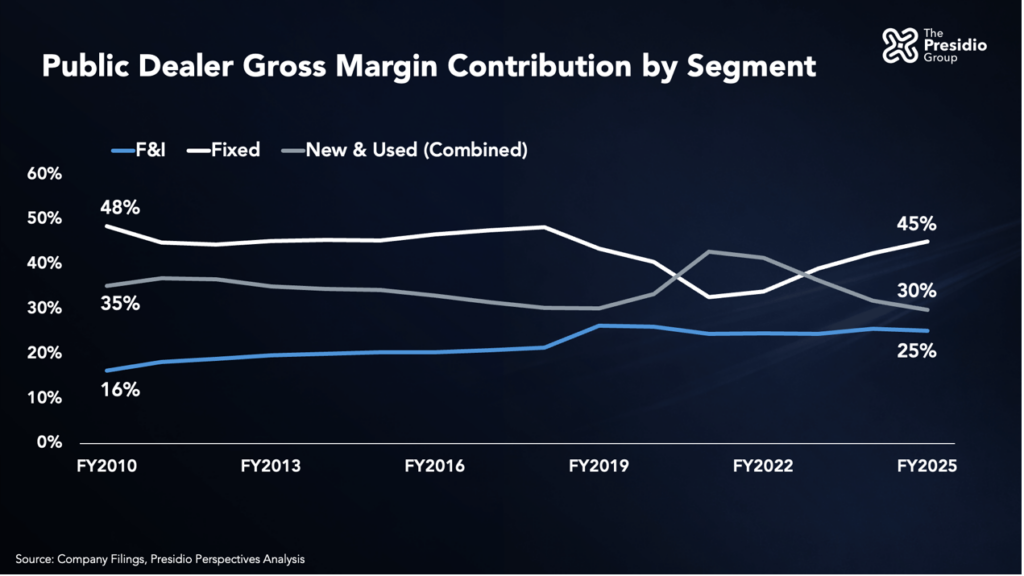

With new and used margin in structural decline, revenue diversification is critical

The public peer group generated $23.5 billion in gross profit in 2025, up 6.4% from 2024. New-vehicle gross margin fell 45 basis points, but gains in used, fixed ops and financial services more than offset the decline, adding a combined $1.6 billion in gross profit. Front-end gross profit per vehicle (new, used and F&I combined) rose 1.7%, driven by F&I at more than $2,000 per unit for the fifth straight year.

For the public dealership groups, gross profit from fixed operations topped $10 billion for the first time in 2025, while F&I delivered a record $5.9 billion. Together, they generated 70% of total gross profit on just 18% of revenue. In 2025, blended gross margin for fixed ops and financial services was 64.7%, while new and used failed to even hold on to a blended 6%.

Diversified dealership model will drive future profitability

The vehicle sales that drive revenue and per-unit gross profit dollars remain linchpins of the franchised dealership business. However, the less-acclaimed financial services and fixed ops segments have become the critical earnings engines as new and used margins resume their structural decline.

Though the new and used segments’ long slide was briefly interrupted by the pandemic, creating an unprecedented financial windfall for automakers and dealers, that structural decline appears to be back. Over the long term, those segments are unlikely to deliver consistent, expanding margins in an increasingly inflationary and competitive industry. The most dependable path forward is a more diversified earnings mix, led by fixed operations and F&I.